WALTER ISAACSON: Staff and patients at Blackpool Hospital in Lancashire England didn’t know it yet, but this was going to be a long day. Early that morning Friday May 12, 2017, the network’s computer monitors flickered, then produced a screen reading oops, your files have been encrypted. This was the WannaCry ransom virus. Below the headline, the screen provided the reader with a convenient FAQ section. The first question in bold red, “What happened to my computer?”, followed by an explanation that the computer’s files have been encrypted, and adding a warning. “Maybe,” read the screen, “you’re busy looking for a way to recover your files, but do not waste your time.” The second question read, “Can I recover my files?” The answer, “Sure.” Then in less than perfect English it warned, “But you have not so enough time.”

In Blackpool Hospital, as in many British health services buildings, health records and emails were frozen. Procedures were canceled, and nonemergency cases were postponed.

At the same time, the WannaCry virus was affecting hundreds of thousands of computers in 150 countries. It struck FedEx, halted production at Renault plants in France, and effectively shut down Spain’s Telefonica and Russia’s postal service. Damage to the economy would be measured in the billions. For each computer system hacked, the ransom was about $300 within three days or $600 within seven days, payable in bitcoin.

Aided by international media and who knows how many Google searches, the world got a crash course in Bitcoin. The words cryptocurrency and blockchain were added to the popular lexicon. The WannaCry virus put a spotlight on one of the many fascinating aspects of Bitcoin. As a digital currency, it’s decentralized. It has no vault or hub or world headquarters. And because it’s so heavily encrypted, Bitcoin transactions are all but impossible to trace. That explains its growing reputation as the unmarked bills in the brown paper bag of the 21st century.

I’m Walter Isaacson, and this is “Trailblazers”, an original podcast from Dell Technologies.

[MUSIC PLAYING]

MAN: What is money anyway?

MAN: Nickels.

MAN: As a medium of exchange for goods.

MAN: Dimes.

MAN: It’s nice to be able to spend what you don’t have.

MAN: Quarters.

MAN: Would you please make out a check to Mr. Frank Adams?

MAN: And half dollars.

MAN: An American loves to consume. It’s in our blood.

WALTER ISAACSON: By the end of the financial collapse of 2008, trillions of dollars worth of household wealth had vanished. The global cost of the collapse would be measured in the tens of trillions. The economic devastation was felt around the world. Little wonder that hardly anyone noticed the release of a nine page white paper by an unknown cryptographer named Satoshi Nakamoto. It was titled “Bitcoin, a peer to peer electronic cash system.”

The first sentence of the abstract described it as a purely peer to peer version of electronic cash that would allow online payments to be sent directly from one party to another. Then came the telling phrase. Quote, “without going through a financial institution.”

Neha Narula is director of the digital currency initiative at the MIT Media Lab.

NEHA NARULA: What we saw with Bitcoin was we saw something that we had never seen before. We saw a way of moving money digitally, so making a payment digitally, without any institutions or banks in the middle. And this was kind of unheard of. No one had ever made a digital payment without a bank before. There was no way to do that. You had to have these trusted institutions kind of sitting in the middle along the path. I would deposit money in my bank account. They would transfer something to a correspondent bank. That would get transferred to potentially another correspondent bank, then to another bank on the other end, and over to my friend that I was trying to pay.

In Bitcoin we eliminate all of those intermediate banks. So I can pay someone directly without any other institutions, companies, organizations being involved. And that’s what was really transformational about it. It was this whole new way of thinking about making payments.

WALTER ISAACSON: Transformational may even be an understatement. Don Tapscott is the co-founder of the Blockchain Research Institution and the author of 16 books on technology, business, and society.

DON TAPSCOTT: Blockchain is the second era of the internet. So the first was the internet of information. And blockchain is the internet of value. The first, if I send you some information, I’m actually not sending you the information. I’m sending you a copy, a PDF, PowerPoint, email. Even with a web site I keep the original. That’s great for information to have a printing press. But when it comes to value, assets that belong to somebody, sending a copy is a terrible idea. If I send you $100 it’s really important I don’t still have the money. Cryptographers have called this the double spend problem for a long time.

So what if there were not just an internet of information? What if there were an internet of value, some kind of, I don’t know, global distributed ledger where anything of value, from money to art to votes, could be stored, protected, transacted, managed, and secured in a private way. And that’s what blockchain is.

WALTER ISAACSON: Before we dig deeper into what Bitcoin and blockchain mean, let’s take a quick tour of how they work. First, how does a blockchain currency, such as Bitcoin, solve the double spend problem? Instead of one central ledger, which could be open to hacking, what if a complete authentic ledger was kept by everyone in a vast worldwide network? That’s what Bitcoin is, a ledger of all transactions shared among thousands of computers worldwide. The keepers of those computers are called miners. The method of keeping that network ledger is called the blockchain. Every 10 minutes, every Bitcoin transaction everywhere is noted and shared as a block with every computer in the network. Those computers also receive an encrypted puzzle.

Imagine computers rolling two dozen dice until one rolls all sixes. The first computer to solve that puzzle wins that particular block, and a proof of solution is shared with the network. That block becomes the authoritative new entry to the network-wide ledger. And the winning miner is awarded new bitcoins. That’s how new bitcoins are produced, or will be until around the year 2140 when the final bitcoin, the 21 millionth, has been mined.

But who can be a bitcoin miner– anyone. But before you take up your virtual pick and shovel, a word of advice. Without the same high tech computer hardware the professional miners use, it could take a thousand lifetimes for you to solve a block on your own.

Bitcoin was and still is an intriguing theory. But for the first part of its lifetime, that’s all it was. That is until the story of the world’s most expensive pizza. Neha Narula.

NEHA NARULA: In those early days, people were downloading software. They were running it. They were becoming part of the Bitcoin network. They were getting bitcoins for being part of that network. They were moving them around between themselves, and it was just all kind of fun.

And then one day, this is what’s sort of thought to be like the real genesis of Bitcoin as money, someone actually bought a pizza from someone else for 10,000 bitcoins. So 10,000 bitcoins, one pizza. Right now today one bitcoin is worth close to $3,000. So you can do the math on how much that pizza cost. It’s pretty crazy.

For the record, as of early this summer, that 10,000 bitcoin pizza would be worth upwards of $26 million. And that’s before you tip the delivery guy.

Meanwhile, new cryptocurrencies are popping up by the hundreds, including one from the industry that effectively pioneered online payment.

[DIAL-UP MODEM]

In the 1990s, the rise of the internet was soon followed by the rise of e-commerce, championed by an unlikely bedfellow, the pornography industry. Porn has traditionally been a serial early adopter. It had boosted the adoption of photography in the 1800s and moving pictures three generations later. It hastened the rise of home video and VCR. For millions, the internet quickly became the plain brown wrapper of adult content. The porn industry not only found ways to monetize their product online, they helped create and refine many of the e-commerce conventions we know today. Pay per click banner ads and real-time credit card processing owe much of their development to pioneers of the adult online industry.

It’s a little wonder then that in 2014 a trio of entrepreneurs released a cryptocurrency specifically for the vending of porn. It creates due payment channels for sellers who might be refused a merchant account by conventional payment apps. For buyers, it leaves no payment trail. Welcome to the era of boutique cryptocurrencies.

In June, Dennis Rodman arrived in North Korea again. This time the trip was underwritten by Potcoin, a cryptocurrency branded for the marijuana industry.

[BONG RIP]

To understand these rapid changes in the way people exchange value, it pays to go back a few thousand years. The first transactions were about trade, usually involving livestock, grain, and produce. I’ll trade you this cow, you give me two bags of grain and a sheep to be named later. [BAA]

In fact, cattle and manure were both used as a form of money. Soon it became practical to use symbols, such as shells or beads, against which the current value of things were measured. Hence the word currency.

Traditional theory has it that money, as we now know it, evolved from barter. Felix Martin begs to differ. He’s a macroeconomist, fund manager, and author of “Money, the Unauthorized Biography”.

FELIX MARTIN: What happens in the beginning is that I give you my fish and you thereby incur a debt to me. And this is a monetary debt. So it’s measured, let’s say, in pounds or in dollars. And I can then use that creditor later, say, to pay someone else with whom I incur a liability in trade. And that system of accumulating credits and debts between people, that’s the essence of the monetary system and offsetting them against one another.

WALTER ISAACSON: Because of the difficulty in carrying a lot of shells or cattle or manure, coins were struck from precious metals. They met the criteria that most currencies would adopt. They were of agreeable value. They were durable. They were distinct and portable.

Over the years, cultures used unusual currencies, from salt cod to animal pelts to playing cards to tally sticks cut from willow. As Neha Narula explains, one of the world’s strangest currencies can be helpful in understanding one of the newest.

NEHA NARULA: I think one way of talking about what Bitcoin is is actually to go back a hundred years and to talk about this culture that lived in Asia called the Yap. Now the Yap’s form of money were these really huge stones. And they didn’t move these stones around the way that we move coins or bills or bars of gold. They left these stones where they were because they were so big. And they just kind of kept track of who owned what stone.

So when one person in the Yap culture wanted to pay another person, they didn’t actually give them a marker of the payment they were making. They just kind of made a note of it. It was, Essentially there was this ledger. And everyone in the Yap society had this collective idea of who owned what. So when we think about money that way, not as an object but instead as this idea that’s kept track of in the minds of people, then we start to think of money as information instead of as something physical.

WALTER ISAACSON: The Yap approach to payment might have been forgotten had it not come to the attention of England’s prestigious “Economic Journal”, which in turn brought it to the attention of one of the country’s greatest influencers. Felix Martin explains.

FELIX MARTIN: They looked at this report of the strange place and they sent it off to a young Cambridge don who was at that time– this was a few years later– serving on war duty in the British treasury. And that young Cambridge don happened to be John Maynard Keynes, the great economist, one of the greatest economist of the 20th century. And he was absolutely fascinated by this story. And he said when he read it, “These people on the island of Yap, they have a much clearer understanding of what money is and how it works than we do today.”

WALTER ISAACSON: Just a few decades earlier as people traded over distances, issues arose around the timing and security of transporting currency. In 1871, Western Union helped resolve those concerns and ushered in an era of analog disruption, using what author Tom Standage calls the Victorian internet. Using the telegraph, they introduced the concept of wiring money. Western Union would accept payment at one of their offices and telegraph a message to another office far afield. That office would surrender that amount to the recipient.

Eight decades later, a moment of embarrassment would inspire a multibillion dollar industry and change the way payments are made. It happened here in New York’s Major’s Cabin Grill one evening in 1949. You may have noticed a well-dressed businessman sitting across from his wife, quietly but urgently frisking himself. That would be Frank McNamara, and he had forgotten his wallet. According to the legend of the night, his wife got the bill and McNamara got an idea. A year later in a moment that has since been dubbed the first supper, he returned to the grill, enjoyed a meal, and at the end presented a small cardboard card as payment. This would evolve into the Diners Club card, the direct DNA ancestor of generations of credit and debit cards that would follow.

Fast forward to today and the dawn of a new virtual currency market. What begin with Bitcoin has blossomed into hundreds of new cryptocurrencies, typically built on the same blockchain technology. But how exactly do they get their value? There was a time when you might have found the answer inside the US Bullion Depository at Fort Knox, just south of Louisville, Kentucky. Prior to the Depression, US currency operated on the gold standard. It could not increase the amount of money in circulation without also increasing its gold reserves. The government partially severed money’s connection to the gold standard in the 1930s to allow for intervention in the economy during the depression.

RICHARD NIXON: We must protect the position of the American dollar as a pillar of monetary stability around the world.

WALTER ISAACSON: Foreign governments could exchange US dollars of gold until 1971, when President Richard Nixon eliminated the gold standard completely. So without gold backing it, what does support the dollar– the same thing that backs cryptocurrencies. Neha Narula.

NEHA NARULA: There’s nothing backing the dollar per se. In fact, if you really think about gold, why is gold so valuable? It’s because we’ve all decided it’s valuable. I mean, gold is certainly useful in certain ways. You can use it in electronics. It makes pretty jewelry. But really gold’s value comes from the fact that people have decided that it’s valuable.

If we can do that with gold, why can’t we do that with a scarce digital asset as well? We have the system, Bitcoin. It manufactures bitcoins out of nowhere but there’s a limited amount of them. And people trade them and they have value because we’ve all decided that they should have value. And it really goes back to this idea of collective fiction. Money is worth whatever we ascribe to it. And I think part of the reason Bitcoin’s worth something right now is because of the potential that people see in it.

WALTER ISAACSON: The end of digital currency put an end to Fort Knox thinking. It’s decentralized. The Fort Knox of Bitcoin is the ledger kept in every one of its network computers. And there’s no vault of precious metal backing them. In this sense, competing cryptocurrencies are waging a battle of the brands where the winning currency will be the one that inspires the most trust.

Digital disruption in payment has many faces, before and after bitcoin. One of them belongs to Max Levchin. While still in college, he helped start a company. His idea? To start a banner advertising network for the then still fledgling worldwide web. The company failed, but its failure only fueled his passion. And he decided to try his hand at a new idea, a security software built for the Palm Pilot, a handheld device all but forgotten. Max Levchin.

MAX LEVCHIN: Summer of ’98 was really hot. And the best air conditioned space within a short walk was the Stanford campus. So I wound up going to a lot of summer school classes and free lectures mostly to just hang out somewhere where it wasn’t hot. Then I saw Peter Thiel, whose name I recognized, giving a talk on currency trading. So I kind of rolled into a class and tried to go as far back as possible to fall asleep in cool. But the class was really small. There are maybe six or seven people in the room in addition to me, and so it really was not polite to immediately pass out.

So I wound up listening and thought, hmm, this guy is really sharp. He’s got a lot of interesting ideas. Wound up chatting him up afterwards. I basically pitched him on two ideas that I had, one of which was a Palm Pilot sort of centric security company. And he thought it was the coolest thing in the world, and basically on the spot said, “Well, I’d like to invest in that.” And almost on the spot I decided, well, instead of you just investing in it, I’m going to try to talk you into being a CEO, because I certainly just want to write code and build cool software. And that’s basically the beginnings of PayPal.

WALTER ISAACSON: And so the idea behind PayPal was born, an application for the Palm Pilot with a very powerful idea at its root.

MAX LEVCHIN: We ultimately settled on this idea, I can pay you, you can pay me, with these kind of electronic IOUs that lived on your Palm Pilot. And it was actually kicking up a lot of press. And there was some excitement.

WALTER ISAACSON: The intent of PayPal was for it to live solely on the Palm Pilot. But as part of their proof of concept, they soon had a web demo of the service running as well. And then Levchin noticed something funny going on.

MAX LEVCHIN: Over time we started noticing that more and more people were playing with it. And at some point there was enough transaction volume, people paying each other through this kind of web demo that I started wondering, well, who are these people? It’s not like we’re promoting the demo. We were promoting the Palm Pilot product. And kind of after a little bit of digging realized that most of them came through this website called eBay. And up until then actually I had never heard of eBay.

And so I sort of thought, well, I don’t know, what is this thing? It’s like a giant garage sale in the sky. I probably should figure out how to shut it down, not let these people from eBay, which all seem kind of suspect, to use my demo. That’s really not what it’s for. And so there was a fair amount of attempt on my part to not just not pivot but actually actively shut down the road to the pivot.

WALTER ISAACSON: The customer base for his company’s Palm Pilot version of PayPal remained static, while the web customer base was growing by 10,000 customers a month. But even then, Max Levchin admits, he didn’t smell the virtual coffee.

MAX LEVCHIN: I was so in love with the Palm Pilot version I actually dragged it out another month or two, just basically refusing to completely kill off the product. And eventually of course killed it. But calling that a pivot is giving pivot a lot of credit. This was a very slow, reluctant move on my part to recognize the market pull that the web version was having.

WALTER ISAACSON: Listening to the pull of the market became a lesson Max Levchin wouldn’t forget. Shortly after going public in 2002, PayPal was acquired by eBay for $1.5 billion.

MAX LEVCHIN: Innovators always have this inherent advantage of nothing to lose and everything to gain by showing up to a market that works well or maybe well enough, but could be much more efficient if things were allowed to be rebuilt from the ground up. That’s what happened at PayPal.

WALTER ISAACSON: Just a few years later, there was a gap in the market that inspired another disruptive new way of paying. It wasn’t so long ago, a maker of hand-blown glass complained that he lost a $2,000 sale because he was unable to accept credit card payments. The friend he was complaining to was Jack Dorsey, whose CV included being one of the co-founders of Twitter. For the two, that became the beginning of Square, a company formed to make credit card payments accessible to more people.

With that, vendors at yard sales or flea markets or church bazaars could accept credit cards, with Square taking a fee from the seller. From food trucks to street vendors, small businesses began adopting Square payment, which gave Dorsey and McKelvey another idea. Square introduced tablet-based payment system for small business with a mobile payment system for customers without the direct involvement of a traditional financial institution.

More than that, it democratizes information. Both the vendor and the customer are provided with data about their purchases. How does weather affect sales? What causes trends in tipping? What time of day can you get the freshest baking or the best deals or find the shortest lineups?

Like cryptocurrencies, these digitally disruptive new payment systems thrive by helping make payments frictionless, and often by removing traditional financial institutions from the role of gatekeeper. In 2001, Andrew Kortina and Iqram Magdon-Ismail were randomly paired as roommates at the University of Pennsylvania. In time they invented Venmo, a strictly peer-to-peer app that has become the go-to for quick friend-to-friend transactions, enough so that Venmo quickly became a verb. You pay the bill for dinner and have your friend Venmo you half the cost.

So in the wake of all this digital disruption, what is the future of payment? From Paypal and Square and Venmo, it’s clear that there is unstoppable momentum in the direction of democratizing payment. But still, it’s arguable that none are as democratic as those that operate in the blockchain, and of course its most famous currency, Satoshi Nakamoto’s Bitcoin.

But just who is Satoshi Nakamoto? Well, technically, he’s the author of the white paper that paved the way for this new internet of value. Strangely enough though, he might not even exist. The white paper is definitely real, and it is known that the paper’s author owns enough bitcoin to live comfortably for several lifetimes. Yet Satoshi Nakamoto has never come forward and never been identified. Many believe the name to be a pseudonym. Maybe it’s more fun not knowing one of the greatest ever strike and fades in digital disruption.

It may be that over time neither Bitcoin nor any one of the new cryptocurrencies reign supreme. It could be something else entirely. But what is undeniable is that we are in the middle of an unstoppable power shift. Money is being democratized. Friction and barriers to payment are vanishing. Banks and traditional financial institutions are beginning to reimagine their future. As earth-shaking innovators go, it’s fair to say that Satoshi Nakamoto is one of the most disruptive.

I’m Walter Isaacson, and this is “Trailblazers”, an original podcast from Dell Technologies. If you enjoyed the show and want to hear more of my thoughts on potential ways that cryptocurrencies like Bitcoin can change the way media creators get paid, visit DellTechnologies.com/trailblazers9. That’s trailblazers then the number 9.

Next episode we’ll be looking at the world of mapping and how a technology like GPS is not only changing the way we locate ourselves in the world but how we communicate with each other as well. You can subscribe to “Trailblazers” in Apple Podcasts or wherever you get your podcasts. And if you like it, please leave us a rating and a review. It helps new listeners discover the show. Thanks for listening.

[MUSIC PLAYING]

After the global economic meltdown of 2008, a mysterious cryptographer, Satoshi Nakamoto, unleashed a nine-page whitepaper on an unsuspecting world. The whitepaper, entitled “Bitcoin: A Peer-to-Peer Electronic Cash System” outlined a future of banking that bypassed financial institutions altogether. Bitcoin became the first cryptocurrency, an entirely new way of moving money digitally.

After the global economic meltdown of 2008, a mysterious cryptographer, Satoshi Nakamoto, unleashed a nine-page whitepaper on an unsuspecting world. The whitepaper, entitled “Bitcoin: A Peer-to-Peer Electronic Cash System” outlined a future of banking that bypassed financial institutions altogether. Bitcoin became the first cryptocurrency, an entirely new way of moving money digitally. But currency has a longstanding history of disruption. From barter, to cattle, to shells, to salt, currency has taken many forms before settling upon coin and paper. Another major recent disruptive development is the story of PayPal, the peer-to-peer payment system that enables online money transfers and empowered the exponential growth of e-commerce.

But currency has a longstanding history of disruption. From barter, to cattle, to shells, to salt, currency has taken many forms before settling upon coin and paper. Another major recent disruptive development is the story of PayPal, the peer-to-peer payment system that enables online money transfers and empowered the exponential growth of e-commerce. And the way we’ve moved money’s changed, too. Western Union and the wire gave way to credit and debit cards – and Square along with it. Digital disruption also aided in popularizing porn and making drugs (briefly) available via Silk Road. From industries as wildly diverse as legalized marijuana and adult film, to startups and food trucks, payment and banking are becoming democratized and more accessible than ever.

And the way we’ve moved money’s changed, too. Western Union and the wire gave way to credit and debit cards – and Square along with it. Digital disruption also aided in popularizing porn and making drugs (briefly) available via Silk Road. From industries as wildly diverse as legalized marijuana and adult film, to startups and food trucks, payment and banking are becoming democratized and more accessible than ever. A Word with Walter

A Word with Walter Neha Narula

Is the Director of the Digital Currency Initiative at the MIT Media Lab. She’s interested in distributed systems, databases, cryptocurrencies, and programmable money. Twitter: @neha

Neha Narula

Is the Director of the Digital Currency Initiative at the MIT Media Lab. She’s interested in distributed systems, databases, cryptocurrencies, and programmable money. Twitter: @neha

Don Tapscott

Is the co-founder of the Blockchain Research Institute. He’s also the author of 16 books about technology and business and society. Twitter: @dtapscott

Don Tapscott

Is the co-founder of the Blockchain Research Institute. He’s also the author of 16 books about technology and business and society. Twitter: @dtapscott

Felix Martin

Is a macroeconomist and a fund manager, and the author of Money: The Unauthorized Biography.

Felix Martin

Is a macroeconomist and a fund manager, and the author of Money: The Unauthorized Biography.

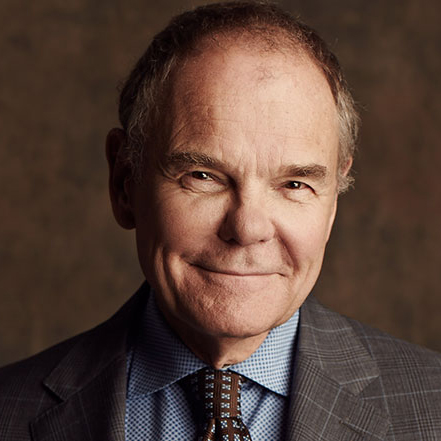

Max Levchin

Is the founder and CEO of Affirm where he hopes to remake consumer finance from the ground up. He is also the chairman Glow, and former Chairman of Yelp. Before all that he co-founded PayPal. Twitter: @mlevchin

Max Levchin

Is the founder and CEO of Affirm where he hopes to remake consumer finance from the ground up. He is also the chairman Glow, and former Chairman of Yelp. Before all that he co-founded PayPal. Twitter: @mlevchin